Laser Guided Growth

A quality small cap riding the demand for more warehousing and automation.

Capital Employed Letter #3

A company going flat-out (excuse the pun) to meet the rising demand for warehousing

Somero Enterprises Inc. is listed on AIM with the ticker SOM.

The company has established itself as the only world-wide supplier of patented, laser screeding equipment, which automates the process of spreading and levelling concrete floors.

Demand for Somero’s equipment is driven by many factors including the need for more warehouse space, rising labour costs, and a shortage of skilled workers.

With the increase in ecommerce and the automation of tasks in the construction industry an on-going structural trend, Somero is well placed to exploit this cyclical tail-wind.

Today’s trading update is very positive, as finnCap writes in its brokers note…

The group has announced a further positive trading update ahead of its December year end, with robust trading in North America by strong demand for new warehousing, with European and Australian operations also seeing strong conditions.

As a result, it is raising its FY21 revenue guidance by 8%, with EBITDA raised 7.2%. It also has increased its year-end cash balance to $39.0m, which boosts dividend prospects.

We upgrade our forecasts in line with guidance and also increase our FY22 dividend by 8.8%.

Today’s news should boost the shares which have been drifting of late and we continue to rate it as a high-quality company with strong trading momentum; on a FY22 P/E of just over 10x and a dividend yield of 7.4% it looks too cheap.

Sounds interesting, lets take a deeper look at SOM.

Please note, this article is meant to act as an introduction to the company and is not a 10,000 word deep dive into every aspect of the company and its accounts. If SOM does pique your interest then make sure you do your own research before buying any shares in the company.

Company Overview

Somero has its global headquarters and training centre in Florida.

It has a production, operations and support hub in Houghton, Massachusetts, with sales offices in Shanghai, New Delhi and Chesterfield (UK).

The origin of the business came in 1984 when Dave and Paul Somero, who ran a concrete flooring business, were asked by customers for a way to make their existing warehouses taller to create more room for shelving and pallets in order to avoid the expense of buying neighbouring land to expand sideways.

In 1997, Summit Partners invested in Somero and brought in a new management team led by Mr Cooney and after listing on AIM at 125p in 2006 the company has gone from strength to strength.

The Products

Somero currently have 18 products. The most popular are the Boomed Screeds and Ride-on Screeds.

Boomed Screeds

From the company website… ‘The boomed Laser Screed products are powerful, easy to transport, and come complete with our full technical support and expertise. So you can make some major efficiency gains on the projects where it matters most.’

Ride-on Screeds

‘With incredible pulling power and the OASIS control system, the S-485 is a ride-on four-wheel drive model that can screed in any direction and is easy-to-operate.’

They also sell remanufactured machines, and software packages such as the 3-D Profiler System® which allows automatic, accurate, paving of contoured sites using Somero® Laser Screed® equipment.

SiteShape System and Floor Levelness System are the other two software apps.

Business Model

The company is much more asset-light than may first appear. While Somero designs and assembles its machines, it outsources the manufacturing to third parties.

This model creates high gross margins and lots of healthy free cash flow.

Somero then sells its screeding machines to property developers. It also provides training, software and maintenance.

The customer base is fragmented and are mostly concrete contractors and self-performing general contractors.

The machines are used in a wide range of projects including:

Warehousing

Industrial/ Manufacturing

Schools/Hospitals

Commercial

Retail

Parking Structures

Somero equipment has been used by many notable organizations including Walmart, Home Depot, B&Q, Carrefour, IKEA, Mercedes-Benz, Coca-Cola, FedEx, and Tesla.

Somero has little customer concentration with customers in over 90 countries. However, North America still makes up the bulk of sales.

Most of the sales are for the Boomed Screeds and Ride-on Screeds which made up nearly 65% of total sales for H1 2021.

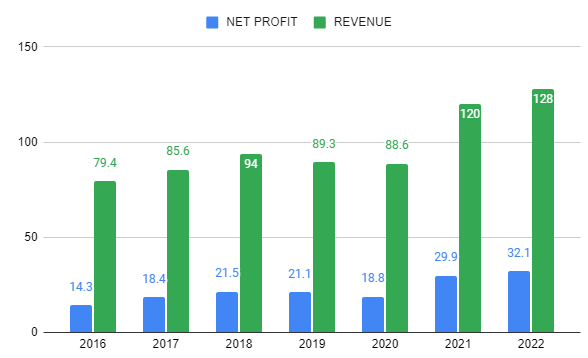

High Quality Metrics

The business is very profitable. Revenue and net profit have been growing steadily.

Operating margins since 2015 have been consistently above 25%. ROCE has averaged 45% since 2015.

Cash conversion has been consistently good, which shows SOM is able to convert a majority of its earnings into cash.

The company has $39m cash on the balance sheet with no significant debt.

SOM operates within a cyclical industry so its good to see a well managed operation, as you never know when the next turn-down in construction may appear.

Competitive Advantages

Somero pioneered the world’s first Laser Screed machine for use in structural high-rise application. The company has both invented and virtually cornered this market. It has minimal competition and owns 97% of the market.

All 18 products are IP protected, and currently holds 73 patents with more in the pipeline. This is a company that’s keen on research and development within the construction automation space.

Due to it’s first mover advantage it works closely with customers, receiving their feedback to improve and create new products, which in turn deepens those relationships.

It provides on-site training, has 24/7 global support in place, and has the infrastructure in place to deliver spare parts in just one day.

This combination of technology, education, and customer support has made barriers to entry slightly higher for any incumbents who want to compete.

Somero places a lot of emphasis on training the users to operate its machines. I don’t know how steep the learning curve is.

However, once someone takes time to learn how to use a Somero machines would they really want the hassle of learning how to use the products of a competitor? This is a nice way of embedding the products into the core infrastructure of their customers business.

Once you learn to design on Adobe Illustrator are you really going to bother to learn to design on another software from scratch?

There is a time switching cost at play here.

Growth Opportunities

With the recent uptick in demand, mainly from the need for more warehousing, Somero is planning a 50,000 sq.ft. expansion of the Houghton facility at an expected cost of $9.5m.

Further opportunities to grow revenue come in two areas -

1 - New products to existing customers and replacing old machines

80% of new orders currently come from existing customers. This comes in the form of customers replacing old worn out machines with the latest generation, and buying new machines that Somero has recently created.

The expected lifespan of the most popular product ‘Boomscreed’ is around 7 to 10 years.

Selling new products to meet the needs of current customers is always a great way to grow with low effort/marketing costs.

The company has introduced three new products to the market in the past two years…

The Somero SkyStrip®, introduced in 2021, replaces manual labor, reduces material damage and improves safety in the process to strip plywood sheets used to shore concrete slabs in structural high-rise buildings.

The Somero Broom+Cure, introduced in 2020, provides an efficient alternative to manual application of curing agents and texture to exterior concrete slabs to comply with American Concrete Institute standards.

The SRS-4, introduced in 2020, is a light weight, remote controlled, easy to transport boomed laser screed machine that provides a solution for hard-to-reach job sites.

The SkyScreed 36, introduced in 2020, is the next generation laser screed machine for structural high-rise applications, providing the operator with reach to screed an additional 1,000 square feet per placement on deck compared to the SkyScreed 25.

2 - Winning new customers via geographical expansion

Establishing local offices will help expansion into new international markets.

They have opened an office in Melboure, Australia. The team down-under grew H1 2021 sales to $2.7m from H1 2020 sales of $0.9m.

India is a big potential market. $1m of sales came from India in 2021, so there is great scope to increase sales here especially as wages rise and more young people choose to work in office based jobs.

China has been a struggle for various reasons. My personal opinion is they should put the Chinese market to one side and focus all their efforts on Europe, India, and Australia for international expansion.

Management

Anyone who invests in UK listed small caps will probably recognise the roster of owners. All popular investment companies with consistent track records.

The current CEO Mr Coody did once own over 6% of the shares but has been slowly selling down over the years, he now owns just over 1%. He hasn’t sold any shares since March 2019.

Mr Coody is 74 years of old. I’m sure at some point the reins will be handed over to someone else. He has done a superb job so it’s always something to keep an eye on when there is a change in management.

Valuation

The shares look good value to me on a variety of metrics.

Judging by the current valuation the market has expressed it’s view as 2020-21 being a one-off jump in profits due to covid19 and subsequent (pointless) lockdowns, which created a speedy need for more ecommerce warehousing.

For this reason it’s difficult to estimate what the growth could be over the next few years.

Broker Finncap had this to say regarding valuation in todays update…

Trading momentum clearly remains robust, and the group has posted a series of upgrades to expectations.

We have a high regard for the group and its management, believing it to deserve a premium rating for its high quality and strong cash-flow characteristics, which then lead to an attractive dividend yield of 7.4%.

We raise our price target by 8.0% to 755p, which offers strong upside to current levels based on a target P/E of 16.3x for FY22, which is not demanding.

The current rating really looks too low, especially after drifting recently, trading on a FY23 P/E of 10.3x, and the shares should react well to this announcement.

Somero is a cyclical company, which is why it trades on a low multiple. However seen from another angle this is also a technology automation company riding the tailwinds of ecommerce and probably deserves a higher rating.

I will leave it with the reader to do their own estimates into future growth and potential valuation.

Risks

There are a few key risks to keep an eye on.

Further Lockdowns

The sales team need to get boots on the ground on the construction sites to show potential buyers how the machines work. Government imposed lockdowns meant the sales team found it difficult to physically showcase their machines. Any newly imposed travel restrictions or closure of building sites will have an impact.

Labour shortages

A shortage of skilled labour has been slowing growth for many of Somero’s customers. However, that does play well into the companies value proposition by offering automation as a solution. As does any rise in the costs of cement.

Rising Interest Rates

When rates are low companies borrow money and build. With higher inflation central banks may be politically forced into raising rates which could dampen construction activity.

The Weather

You obviously can’t lay concrete in wet weather. The highest rainfall recorded in over 120 years between May 2018 and April 2019 accompanied by insane blizzards in the US did hold the company back.

The weather of course is in the lap of the gods so not much the company can do about it. Luckily so far this year the weather has not caused any problems/delays in construction activity.

Conclusion

The investment thesis for Somero is simple. The company is well managed, has high operating margins, good returns on capital, pays a chunky dividend, and is riding the trend of ecommerce, storage, and construction automation.

With more products in the pipeline, and growth in international sales, SOM could be a steady grower over the next five years.

However, it’s customer base in the US is susceptible to an increase in interest rates, and key management roles will need replacing at some point.

I feel the the valuation has taken much of this into consideration, so it could be a good buy at this price.

Witten by Jon Kingston

@equitybaron on twitter.

References/Further Reading

https://investors.somero.com/investor-contacts

Disclaimer

The above article is for informational and educational purposes only, and should not be seen as investment advice. Please do your own research before thinking of investing in any company mentioned.

Sorry also where did you find that 80% of new orders are from existing customers? I am also long SOM and have done significant amount of research however haven't found either of these stats. Even more bullish now however! thanks again for a great article

Thanks for the article - where did you source the stat of 97% market share as I haven't seen before?