2 Stock Pitches by Patrick Rial (TriVista Capital/Hosomichi Fund)

Interview #134 - Discusses background, investment style, and pitches two Japanese small caps.

For this edition we welcome Patrick Rial from TriVista Capital/Hosomichi Fund.

Patrick discusses his background, approach to investing, and shares two stock ideas.

(Disclaimer: This interview is for informational and educational purposes only, and should not be seen as investment advice. Please do your own research before investing in any company mentioned).

Hi Patrick, thanks so much for taking the time to do this interview.

Can you please tell readers about your background, and how you got involved in investing?

Hi Jon. Thanks so much for this opportunity. I am a big fan of Capital Employed and have discovered a number of interesting Japanese stocks here.

I am an American but have been living in Japan for 23 years. My original goal was to be a journalist; I fancied myself the next Malcom Gladwell and dreamed of writing for The New Yorker. Unfortunately, I graduated in the early 2000s, just as print journalism embarked on a never-ending structural decline.

I couldn’t find a job in journalism, so I came to Japan to work as an English teacher on the premise that if I waited a year maybe the Internet would disappear and the industry would come roaring back. I am still waiting for this thesis to play out!

My interest in Japan dates back to my obsession with the Karate Kid movies. In the early 2000s I even tracked down Ralph Macchio and went to his home on Long Island. He was not happy about that! But he did take a photo with me and sign my VHS tape if I promised never to come back.

“Best Wishes! - Ralph Macchio ‘01”

I started doing karate, taekwondo and kung fu in high school and college, and so always had a strong interest in Asia, and Japan in particular. When I arrived in Japan, I was surprised to learn karate is just as dorky here as it is in the U.S. So, I hung up my gi and took up rock climbing instead.

Still, I fell in love with Japan and decided to stay. I started working as a freelance journalist, but it wasn’t sustainable. I ran through my savings and had to ration myself to a single daily visit to the convenience store for food.

I landed a job as a reporter at Bloomberg just in the nick of time. I remember they apologized for the “low” salary offer of $50k, not knowing I would have said “yes” if they offered me a day-old taco.

Bloomberg exposed me to investing. Your readers already know that investing is the most fascinating, endlessly-permutating puzzle out there. I was hooked.

At some point, I realized I was not getting any closer to writing for The New Yorker. And anyways, finance had become more interesting. When I grumbled about my situation to a friend at Morgan Stanley, he offered me a job. I became a product manager, where I used my experience as a journalist to help analysts write reports that stand out in a crowded field.

Morgan Stanley was the platonic ideal of a company: intelligent, high-quality people working in cooperation towards a common goal, and having a lot of fun along the way. I couldn’t have asked for a better environment.

However, as I studied Graham, Buffett and others, my goal changed to becoming part of the decision-making on the buy side, rather than the advisory side. That meant I first needed to learn how to be an analyst.

I’d met the head of research at J.P. Morgan during my journalism days, and when I reached out, he offered me a job as his junior analyst. I covered macro strategy and small cap research.

Ironically, my years doing macro strategy helped cure me of trying to predict the macro; there are too many moving parts for the human mind to comprehend, in my view.

Small cap stocks were the polar opposite. They are easy to understand, and the likelihood of mispricing is inversely proportional to the number of eyeballs on the companies. Japan is blessed with nearly 3000 listed small caps to choose from.

The day after my mentor quit J.P. Morgan, I received an email from the founder of Varecs Partners, whom I had met a few months earlier. I joined Varecs, a value-oriented boutique fund influenced by First Eagle and Buffett, as an analyst in 2015.

I spent the next 10 years honing my skills researching overlooked Japanese companies. Being an analyst is nearly identical to being a journalist, with just a bit more math.

We had a lot of fun at Varecs digging up hidden gems. However, I left at the end of 2025 to pursue my dream of becoming a fund manager.

Maybe it is worth noting for some of your younger readers, I have not formally interviewed for a job in 20 years. My network of friends and colleagues have been the source of every new opportunity.

One of the best things you can do for your career is to be a team player, help others, and make friends. I had a strong competitive drive when I started out, a vestige of my Western upbringing. But I have found you are better off trying to be helpful than trying to come out on top.

You will be shocked by how coworkers and others you meet when you are young start to rise to positions of influence. If you treated them well, they may lend you a hand later on. Your former intern may become a CEO or a country head. I’ve seen it happen many times.

Can you provide readers with a brief overview of the Hosomichi Fund?

The Hosomichi Fund is in pre-launch phase and expected to start in September. I am partnered with the excellent folks at TriVista Capital in Tokyo and will launch under their umbrella. This setup frees me to focus the maximum amount of time on running the fund, and minimal time on operations.

The strategy is small cap, constructivist and focused primarily on people. We eschew the typical screening approach. We believe that the quality and drive of the people running the company, combined with the culture they create, ultimately determines your return.

The industry and “moat” are secondary, in my opinion. I am skeptical of the very concept of “moats” as distinct from the people working at the company.

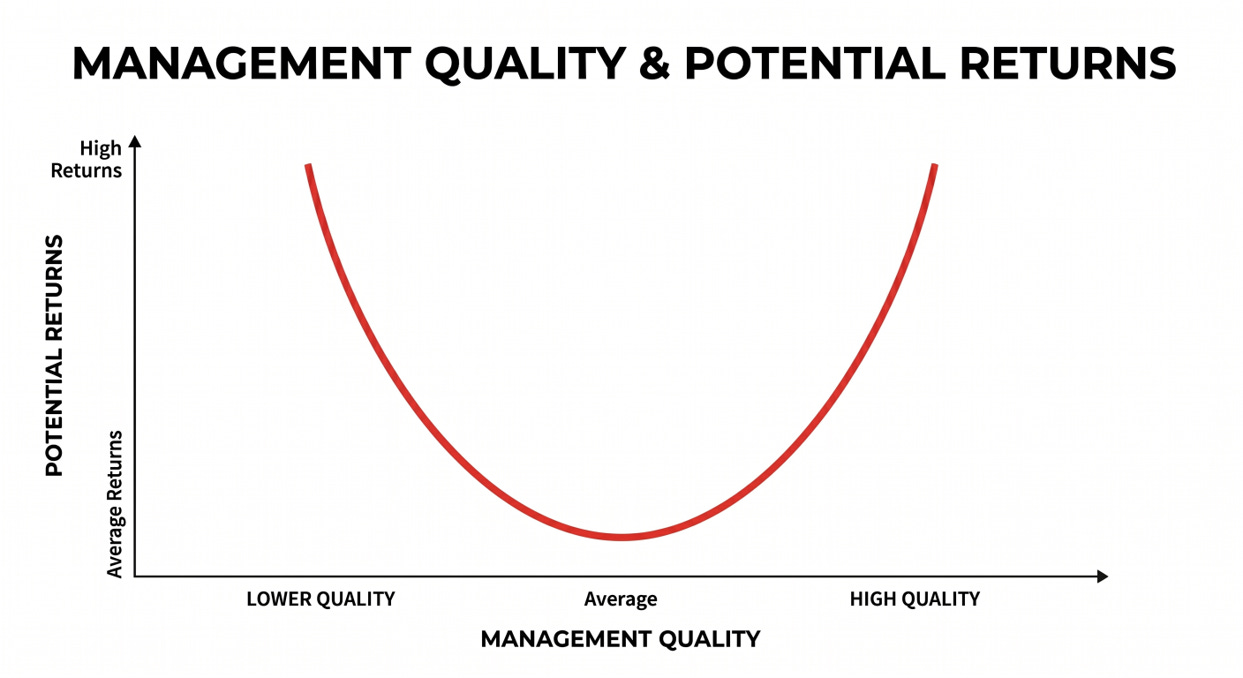

Outsized returns are hard to come by, but I am focused on 2 winning patterns I have identified:

Source: TriVista Capital

Exceptional returns can be found investing in both the lowest and highest quality management teams.

Companies managed by lower quality teams trade at depressed multiples. Intervention by an engaged shareholder can catalyze improved performance on multiple fronts: balance sheet management, employee motivation, sales growth and innovation.

That can result in a significant re-rating. Of course, most management teams are not enthused about breaking with old patterns. We always approach the company in a friendly manner, but friendship is a two-way street. At the end of the day, we will take measures to safeguard investor capital.

Meanwhile, the highest quality management teams also tend to be structurally undervalued, even if they trade at comparable multiples to peers. The best managers will grow faster, attract better talent, and treat shareholders better than rivals.

They thus deserve to trade at a premium. While such managers are exceptional operators, in Japan they tend to be somewhat ignorant of capital markets. Our approach is to work with these companies to set ambitious financial goals, devise M&A strategy, and help tell their story to investors.