2 Stock Ideas by David Ridland (Castlebay Investment Partners)

Interview #135 - Discusses investment style, value in the UK, and presents the investment case for two very interesting UK stocks.

For this edition we welcome back David Ridland from Castlebay Investment Partners LLP.

(Disclaimer: This interview is for informational and educational purposes only, and should not be seen as investment advice. Please do your own research before investing in any company mentioned).

Hi David, We last spoke in 2021, a lot has happened since then. Have you made any tweaks or changes to your investment approach or style?

Jeff Bezos was once asked what he thought would change in the next ten years. He said the more interesting question is what stays the same!

For us, in investing, the answer is straightforward: Quality, value - in that order. We don’t want to overpay for the privilege of owning a great business; and we won’t get in the way of the compounding returns those businesses make for us over time.

That principle hasn’t changed since we launched the fund. Having said that, we are always trying to get better and evolve. We’ve never been comfortable standing still analytically.

Over the last few years having developed an analytical database, called Wayfinder, we have sought to enhance its capabilities. Recently, we have developed our Fund Intelligence Dashboard, the greatest benefit of which is to maximise our ‘thinking time’ through efficiently gathering and analysing the critical factors underpinning our investment theses.

One of the most important developments to our analytical toolkit has been what we call cashflow lifecycle analysis. The insight is deceptively simple: the right capital allocation behaviour looks very different depending on where a business sits in its lifecycle; and the market is often slow to notice when management gets this wrong.

A young, high-growth business should be reinvesting aggressively its free cashflow back into the business. We expect capital intensity to be higher than at other stages and we understand that. However, a mature business that has passed its peak growth phase should be doing something very different: harvesting returns, generating cash and returning it to shareholders.

When we see a mature company chasing growth — acquiring at inflated prices, building capacity into a saturated market, leveraging up to fund expansion — that’s a significant warning signal. The market tends to reward the activity initially, because growth is instinctively appealing. We’ve learned to be sceptical of it.

What cashflow lifecycle analysis gives us is a systematic framework for identifying these behavioural mismatches early — before their effects are felt in reported earnings and hopefully before the share price responds.

A management team allocating capital well through the lifecycle of their business is creating shareholder value quietly and consistently. Yet, through the wrong incentive structures, management can destroy value, often whilst appearing to grow earnings in the short term.

The two systems work together. The valuation discipline of Wayfinder sits alongside the quality surveillance and lifecycle analysis of the Dashboard.

Between them they answer the questions that matter most: is this still the business we thought it was, is management stewarding capital the way we’d expect at this point in the lifecycle and are we still paying a sensible price?

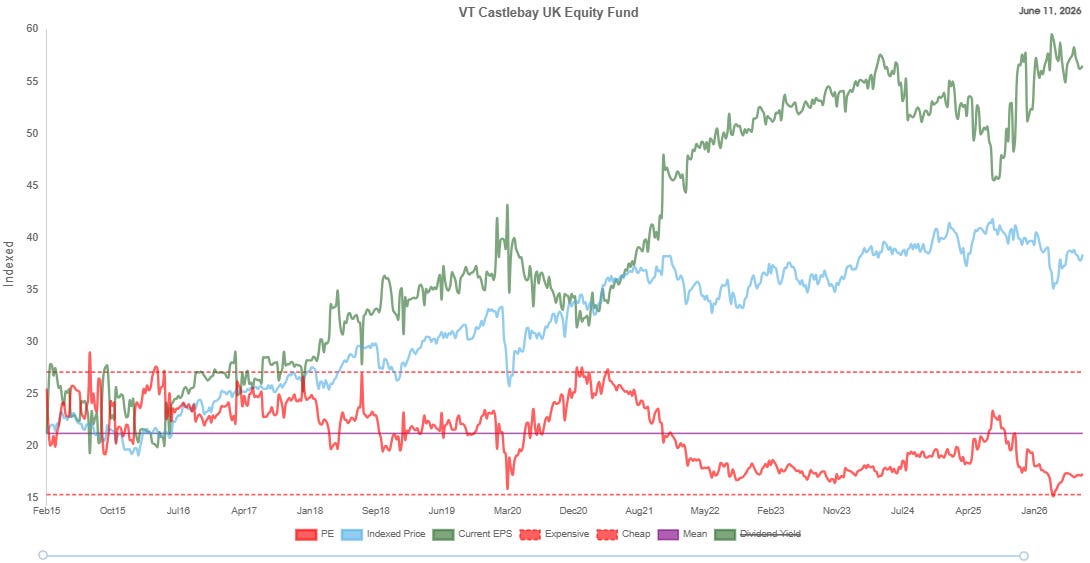

The average free cash flow yield for your fund is 6%, and the dividend yield 4%. I was quite surprised to read that. Is this the highest they’ve been since you launched the fund?

Yes. And the surprise you feel reading those numbers is, I think, the right reaction.

Look at the valuation graph below. The red valuation line hit the extreme valuation point (the lower dotted red line), at the end of March this year. That’s when the free cashflow yield hit 6%. It often seems to us that valuation means less ‘in the middle’. It is at the extremes when it most impacts future returns.

Our average return on equity is 35% — more than double the market average. Our operating margins are 24% against 17% for the broader market. These are not ordinary businesses. They generate cash with a kind of efficiency that most companies never achieve; and the market is currently pricing that cash as if it were unremarkable.

To your question about whether this is a record - yes it is. When we launched our fund in January 2015, quality compounders were in vogue and you paid a premium to own them. It took us five years to become fully invested in the fund as we didn’t want to overpay for these quality companies.

Over recent years, the narrative has shifted. Investors have rotated toward lower quality companies — toward cyclicals, commodity producers, financials. The businesses we own, which compound quietly and consistently, are sitting in the waiting room while noisier assets attract the crowd.

“A 6% free cash flow yield on businesses with a 35% return on equity. The market is pricing these compounders as if the compounding will stop. We don’t think it will.”

The dividend yield tells a similar story. 4% from a portfolio of quality growth businesses is rare. These companies pay dividends from genuine surplus cash — after reinvesting in the business, after maintaining the balance sheet, after funding organic growth. That’s a very different 4% from a company paying out more than it earns.

Perhaps things are changing though? From the end of March, as of writing, our fund has risen by 10% - outperforming our peers and the market by some margin. Whilst the free cashflow yield has fallen to 5.6% and the dividend yield to 3.7%, strong operating results from our companies have helped maintain these compelling valuations.

In short, valuations are still at the extreme, all while our companies continue to deliver double digit earnings and cashflow growth. (11% annualised earnings growth over the last 5 and 10 years.)